Last week, we discussed in broad strokes the importance of durable competitive advantage — or what Warren Buffett popularised as business moats.

We briefly mentioned that the concept of a moat does not yield itself to easy algebra — you must blend the quantitative with the qualitative.

As Buffett once noted regarding attempts to take precise measurements of a moat (emphasis added):

‘There’s no formula that gives you that precisely, you know, that says that the moat is 28 feet wide and 16 feet deep, you know, or anything of the sort.

‘You have to understand the businesses.

‘And that’s what drives the academics crazy, because they know how to calculate standard deviations and all kinds of things, but that doesn’t tell them anything.

‘And that what really tells you something is if you know how to figure out how wide the moat is and whether it’s likely to widen further or shrink on you.’

You must understand the businesses themselves. You can’t approach them tangentially by only looking at the price chart or a few ratios.

That won’t give you a true sense of what the business does and how it operates.

And that’s why Buffett and his investment partner Charlie Munger consider themselves business analysts first and foremost:

‘When investing, we view ourselves as business analysts — not as market analysts, not as macroeconomic analysts, and not even as security analysts.’

So what is a good business?

What is a business with a wide and durable competitive advantage?

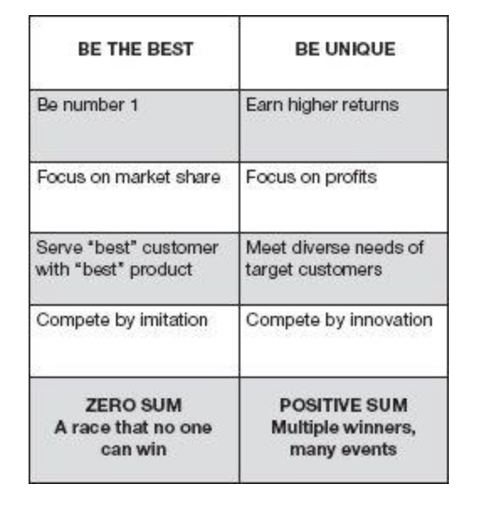

Having a business moat is not the same as being the best

A common mistake is thinking strategy is about beating your rivals. And therefore, the companies with the biggest moats are the ones with the most vanquished competitors.

But a competitive advantage lies in being unique, not being ‘the best’.

Think about this.

What is the best car?

What is the best smartphone?

What is the best restaurant?

Often, what is considered the best in these categories depends on the customer and their preferences.

Michael Porter — who has done much to advance the study of competitive advantage — thinks the ‘competition to be the best’ is misguided.

In Porter’s view, it is absolutely the wrong way to think about competition.

As Joan Magretta wrote in her Understanding Michael Porter:

‘Think about all of the industries in the economy. In how many does the idea of “being the best” make real sense?

‘In most industries, there are many different customers with different needs. The best hotel for one customer is not the best for another. The best sales encounter for one customer is not the best for another. There is no best art museum, no one best way to promote environmental sustainability.

‘The best always depends on what you are trying to accomplish. Thus, the first flaw of competition to be the best is that if an organization sets out to be the best, it sets itself an impossible goal.’

As we mentioned last week, maybe Peter Thiel was onto something when he wrote that competition is for losers.

|

|

|

Source: Joan Magretta (2012) |

Warren Buffett and business moats

Another insidious upshot of competition is what Porter dubbed competitive convergence.

If you fixate on beating your rivals, you begin to resemble them.

That’s not a good thing.

When rivals focus on doing better than everyone else is doing, they converge on the same ideas, practices, and models.

You can stand out with your execution, but not your thinking.

As Magretta explains:

‘Everyone in the industry will listen to the same advice and follow the same prescription. Companies will benchmark each other’s practices and products. Competing to be the best leads inevitably to a destructive, zero-sum competition that no one can win.

‘Over time, rivals begin to look alike as one difference after another erodes. Customers are left with nothing but price as the basis for their choices.’

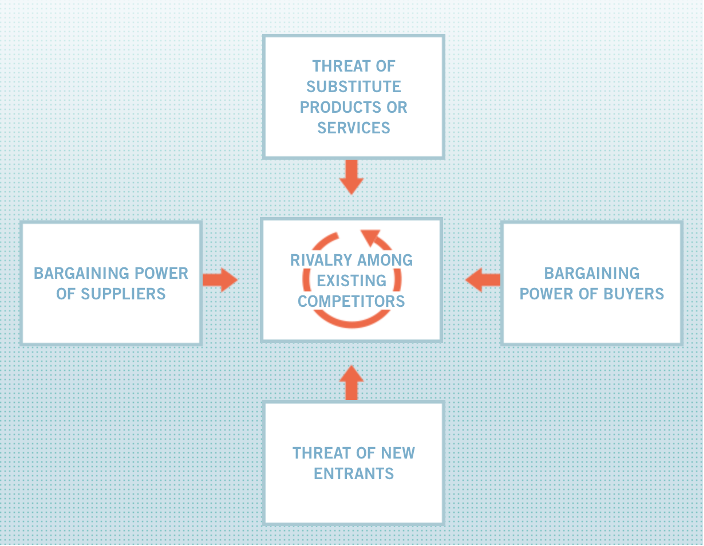

The types of competitive advantage: Michael Porter’s five forces

What are the different types of competitive advantage?

What does a business moat look like?

The most famous conception of competitive advantage stems from work by Michael Porter.

Through his years of research, Porter came up with five forces that he thinks account for the competitive advantage universe.

Here are the five factors:

Threat of substitute products or services

A substitute is another service or product that meets the same wants or needs that an existing product satisfies in a different way.

A common example is email being a substitute for posted mail.

Another example we wrote about elsewhere is the alternatives to lithium-ion batteries.

If lithium prices remain elevated, manufacturers might seek out battery metal substitutes and alternative battery chemistries.

Bargaining power of suppliers

Businesses don’t exist in a vacuum. They interact not only with customers but with other businesses, too. That includes suppliers who provide the inputs a business turns into products.

Some industries may have powerful suppliers who can negotiate favourable prices for themselves and thus shrink a business’s margins.

This is often associated with Amazon, which is sometimes called in economics parlance a monopsony power. Amazon is a large supplier of retail goods, frequently making its bargaining position with sellers lopsided. For an example, see the long-running dispute between Amazon and book publisher Hachette.

Threat of new entrants

This is likely the most well-known competitive force influencing competitive advantage, also described as barriers to entry.

If a business operates in a sector where the threat of new entrants is high — and barriers to entry are low — it will have to keep prices down while spending more to retain customers for fear of losing them.

Think of your local coffee shop. What is the threat of new entrants? For that matter, how live is the threat of substitute products? With living costs up, will customers turn to instant coffee, tea, or flavoured milk?

Bargaining power of buyers

Similar to the bargaining power of suppliers, the bargaining power of buyers refers to the leverage customers have over a business.

Powerful customers can throw their weight around and force prices down.

The bargaining power of buyers increases the less differentiated a product is or when switching costs are minimal.

A sector where buyers can pit competing firms against each other is one where the bargaining power of buyers is high.

Rivalry among existing competitors

This relates to Porter’s ‘competition to be the best’ syndrome, where rivals engage in a zero-sum battle where a gain for one business is a loss for another.

If rivalry is heated, prices are driven down to the cost of capital, and profits are few and far between.

For Porter, rivalry is especially fierce if:

- Competitors are numerous and of similar size

- Industry growth is slow

- Exit barriers are high

- Rivals are committed to the business

|

|

|

Source: Michael Porter |

Morningstar’s five business moat sources

Of course, Porter’s taxonomy of competitive advantage isn’t definitive. Partly because — as Buffett noted — the subject doesn’t lend itself to rigid quantitative boundaries.

We have multiple ways to analyse moats…

Like the way espoused by large investment research firm Morningstar, which pioneers its own moat ranking method.

Morningstar argues there are five business moat sources. They are:

Intangible assets

‘Intangible assets include brands, patents, or government licences that explicitly keep competitors at bay.’

Cost advantage

‘Firms that have the ability to provide goods or services at lower cost have an advantage because they can undercut their rivals on price. Alternatively, they may sell their products or services at the same prices as rivals, but achieve fatter profit margins. We consider economies of scale to be a type of cost advantage, an idea we discuss in more detail in the next chapter.’

Switching costs

‘Switching costs are those one-time inconveniences or expenses a customer incurs to change from one product to another. Customers facing high switching costs often won’t change providers unless they are offered a large improvement in either price or performance, and even then, the risk associated with making a change may still prevent switching in some industries.’

Network effect

‘The network effect occurs when the value of a particular good or service increases for both new and existing users as more people use that good or service, often creating a vicious circle that allows strong companies to become even stronger.’

Efficient scale

‘Efficient scale describes a dynamic in which a market of limited size is effectively served by one or just a few companies. The companies involved generate economic profits, but potential competitors are discouraged from entering because doing so would result in insufficient returns for all players.’

Assessing the business moat of BNPL stocks

Let’s quickly apply the principles we’ve covered above to the ‘buy now, pay later’ industry.

The BNPL sector is interesting because it was often heralded as a momentous change in how we pay and was even considered a threat to traditional banks.

But as Buffett said, it’s not necessarily the societal impact or growth of an industry but the durable competitive advantage of a business that counts.

So does the BNPL model stack up? Do any ASX BNPL stocks have a durable competitive advantage?

Threat of new entrants

One of the biggest challenges for standalone providers is the threat of new entrants.

The new entrants can be fellow standalone BNPL newcomers but also big legacy players like PayPal or Visa or the Big Four banks who roll out their own instalment options.

The barriers to entry are not high, and rivals — seeing the rapid BNPL uptake by customers — flooded the sector.

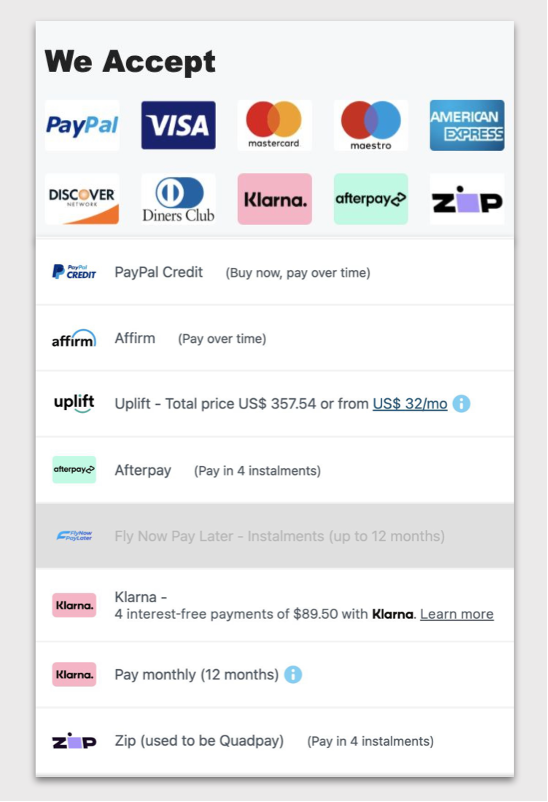

Even fellow BNPL stock Splitit admits this, wishing to differentiate itself from ‘legacy BNPL providers’. In a presentation earlier this year, Splitit acknowledged the crowded BNPL market, sharing the following illustrative snapshot:

|

|

|

Source: Splitit |

A durable moat protects a business from new rivals. The existence of many competitors implies the moat is narrow and shallow.

As Buffett explained:

‘We think of every business as an economic castle. And castles are subject to marauders. And in capitalism, with any castle…you have to expect…that millions of people out there…are thinking about ways to take your castle away. Then the question is, “What kind of moat do you have around that castle that protects it?’

Switching costs/bargaining power of buyers

As a product, BNPL is not unique.

What does Zip offer that materially differs to what Splitit or Sezzle or Klarna or Afterpay offer?

Yes, some BNPL companies specialise in offering instalments for larger purchases, some for special categories like vet visits or auto services…

But in the end, what BNPL stocks offeris the ability to make a purchase — of whatever size or whatever kind — in instalments.

As a result, switching costs are minimal; loyalty is lacking.

Splitit itself noted the ‘cost of acquiring new customers is increasing exponentially and lack of consumer loyalty as 70% of BNPL users would switch providers’.

Competitive convergence/rivalry among existing firms

The lack of differentiation between firms and the constant threat of new entrants makes the rivalry between existing BNPL firms intense.

Not only that, the BNPL firms have seemingly committed the grave mistake of competing to be the best.

In this competitive rat race, the BNPL firms converged on a strategy we have come to know well — hypergrowth at all costs.

For years it worked well, as investors were impressed with rising transaction volume, customer growth, and merchant sign-ups.

But in the race to be ‘the next Afterpay’, the BNPL sector became overly homogeneous.

Yet it’s in uniqueness that profits lie.

As Joan Margetta quipped:

‘There is no honour in size or growth if those are profitless. Competition is about profits, not market share.’

Regards,

Kiryll Prakapenka,

For Money Morning