Natural beauty and wellness retailer BWX’s [ASX:BWX] shares plummeted after revealing a heavily discounted capital raising and mixed trading outlook.

BWX shares fell nearly 40% by late afternoon trade on Tuesday. The BWX stock is now down 85% over the past 12 months.

The stock reached as high as $5.56 in June 2021 but is now hovering at around 70 cents:

Source: TradingView.com

BWX capital raising to cut back debt

BWX has tapped investors to help with its debt by issuing new shares at a heavy discount.

Looking to reduce debt at a time of rising interest rates, BWX announced a fully underwritten $23.2 million capital raise.

BWX’s two big investors — Bennelong Australian Equity Partners and Tattarang — will participate. The duo already owns about 40% of the beauty retailer.

The capital raise will break down into a $13.5 million placement to sophisticated and professional investors and a further $9.7 million ‘1-for-10’ non-renounceable entitlement offer.

BWX reported that its pro forma net debt as of 30 June 2022 is expected to be in the range of $58–62 million.

BWX estimates that its pro forma net debt will shrink to $23 million by June 2023.

The retailer will be offering fully paid ordinary shares underwritten at 60 cents a share, which represents a hefty 48.7% discount to its 23 June closing price of $1.17 each.

Around 38.6 million new shares will be issued, which is about 24% of BWX’s existing shares on issue.

BWX said its primary lender the Commonwealth Bank is ‘supportive of the capital raise’, and has agreed to suspend BWX’s financial covenant obligations for the periods ending 30 June and 30 September 2022.

Changes to guidance

BWX also took the opportunity on Tuesday to update its revenue and earnings guidance.

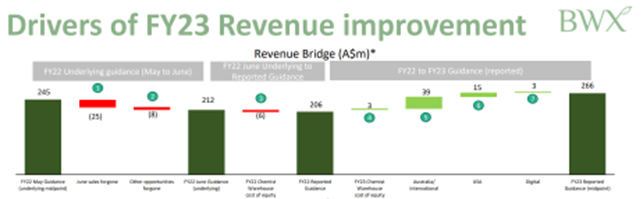

BWX now expects FY22 revenue to rise 6% on FY21, up from $194.1 million to $206 million.

It was only last month the retailer was forecasting FY22 revenue to be between $233–243 million.

EBITDA is now expected to fall 76% from FY21 to $6–10 million, down from FY21’s $33.4 million.

Last month’s guidance was for FY22 EBITDA to be in the range of $27–30 million.

BWX expects to make a net loss of $10–14 million in FY22.

Interestingly, BWX expects a rebound in revenue and EBITDA in FY23.

FY23 EBITDA is expected to jump a whole 488% on FY22 to $45–49 million on a 29% increase in revenue to $260–270 million.

Four new non-executive directors are expected to be appointed in November — a decision that will be subject to shareholder votes.

What has happened between May and June to warrant the drastic cut in EBITDA and revenue guidance?

BWX blamed a ‘one-off impact’ of removing planned June sales due to ‘changing market conditions’.

BWX also cited ‘other opportunities missed in June’.

Source: BWX

BWX share price outlook

Commenting on the swift change in guidance, BWX said:

‘Retail conditions are more challenging with increasing inflation, interest rate increases and a much more cautious consumer.

‘When we provided a trading update in May, our plans assumed selling into and holding a certain level of inventory with select wholesalers and retailers in June.

‘The challenging market conditions have caused us to change our approach.

‘The terms of trade associated with the previously planned sales are no longer in the Company’s best interests.’

BWX said it will now prioritise reducing its debt, divesting from non-core assets, and reducing inventory by $20 million.

The downgrade comes at a time when with analysts are predicting tough times ahead for retailers, as rising interest rates are set to curb consumer spending and increase retailers’ cost of debt.

With consumer spending expected to retrench, retailers may also face an inventory issue — with overstocked shelves set for discounted sales — and lowered margins.

While it’s certainly a challenging time for stocks right now, opportunities still exist.

And our expert Callum Newman has a knack for spotting them.

Last week, Callum released a fresh report on three overlooked battery stocks that could be some of the most exciting nickel projects in the world.

I highly recommend you check out his report here.

Regards,

Kiryll Prakapenka,

For Money Morning