Lithium miner Pilbara Minerals Ltd [ASX:PLS] fell on Wednesday after releasing its June quarter production and sales update.

Despite a significant increase in June quarter production, the lithium stock was trading down 2.5% in late afternoon trade.

PLS was unable to buck the trend, with plenty of lithium stocks falling sharply on Wednesday.

At the time of writing, Sayona Mining [ASX:SYA] was down 11%.

Ioneer [ASX:INR] was down 9%.

Leo Lithium [ASX:LLL] was down 9%.

Li-S Energy [ASX:LIS] was down 10%.

And Arizona Lithium [ASX:AZL] was down 8.5%.

Year to date, PLS shares are down 25%.

Source: Tradingview.com

Pilbara’s ‘significant’ production increase

Pilbara announced a ‘significant’ 54% increase in June quarter spodumene concentrate production.

PLS estimates its June quarter production to be between 123,000 and 127,000 dry metric tonnes (DMT), a big jump on the March quarter production of 81,431dmt.

Estimated shipments for the June quarter have increased 118% from the March quarter, up from 58,383dmt to between 127,000 and 132,000dmt.

PLS now expects FY22 annualised production to be in the range of 373,000 to 377,000dmt, a 33% increase on FY21.

The company also expects FY22 shipments to increase 26% on 2021’s total, to be in the range of 335,000 and 360,000dmt.

As of 30 June, Pilbara estimates its cash balance to be in the range of $850 million to $855 million.

Pilbara’s cash balance for June 30 has estimated within the AU$850 to AU$855-million range, including AU$269 million in bank credit letters.

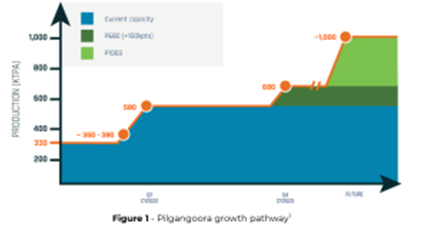

Pilbara is hoping that its Ngungaju Plant will increase capacity to 180–200,000 tonnes a year for the September Quarter, which will play into the Pilgangoora Operation capacity run-rate of 540 to 580,000 tonnes a year.

Pilgangoora Production FID

Along with its cash and shipping updates, Pilbara also announced that it has closed its Final Investment Decision geared towards a production increase at the Pilgangoora Operation — it’s P680 Project.

The P680 Project should result in an increase from 580,000 tonnes a year of spodumene concentrate to 680,000.

A further 100,000 tonnes a year is expected from circuits which reject low-grade waste materials, at a capital cost estimate of $103 million.

Another $194 million in capital costs would see up to 5 million tonnes of ore a year crushed by its new sorting facility, then increasing production around 640–680,000 tonnes a year.

The company expects the Primary Rejection commissioning venture, which Pilbara joint-owns with POSCO, to commence after the September Quarter 2023.

PLS’ incoming CEO, Dale Henderson, said:

‘This is an exciting milestone for Pilbara Minerals. It reinforces the exceptional scale and quality of our Pilgangoora Project, which is one of the few hard rock lithium production operations globally that has both the resource size and existing operating platform to enable a rapid scale-up of production to meet our customers’ long-term requirements.

‘From the outset, our long-term growth strategy has been to develop each stage with a focus on tailoring production to meet demand, while also planning for future expansion opportunities.

‘Following the Board’s Final Investment Decision, we are now able to commence construction of the P680 Project in the coming months and expect commissioning of the primary rejection facility during the second half of next year with the crushing and ore sorting facility to follow shortly thereafter.’

Source: PLS

PLS share price outlook

Despite the strong production figures, Pilbara did not some inflationary pressures.

Its unit cost guidance for concentrate shipped from the Pilgan operation during the June quarter has been bumped up to between $650–680/dmt.

Previous guidance released in April was for unit costs to be in the range of $490–530/dmt.

During the March quarter, unit costs were $632/dmt.

Plibara elaborated:

‘Inflationary pressures have been encountered by the Company during the Quarter, with a 40% increase in net diesel fuel prices compared to the March Quarter (and negatively impacted by the short term 50% reduction in the fuel tax rebate).

‘In addition, higher reagent costs (including related logistics) and labour costs associated with the buoyant labour market for the WA mining industry (inclusive of bonus structures to attract and retain employees) also contributed to cost increases.

‘The impact of COVID-19 affected the number of personnel on site and, ultimately, impacted operational performance.

‘Unit costs were also impacted by the absence of tantalum production during the Quarter, as the operations deliberately targeted ore feed from the South Pit to maximise lithia units to take full advantage of favourable market conditions.’

Now, as EV adoption ramps up, car manufacturers are scrapping a five-decade-long pattern of outsourcing to tighten supply chains by seeking partnerships all along the supply chain to secure supply.

Chief among them is Tesla, seeking deals with several EV battery resource companies, some of which are based here in Australia.

Our small-cap expert Callum Newman believes the rush to secure battery materials isn’t over yet.

He thinks there are ASX stocks flying under the radar who could be the next ‘chosen ones’ — stocks tipped by Tesla to be their battery materials supply partners.

Callum thinks that one of the three battery stocks in his latest report ‘could be one of the most exciting nickel projects in the world. I’m not kidding’.

To find out more, read Callum’s latest battery materials report, ‘Elon’s Chosen One’, here.

Regards,

Kiryll Prakapenka,

For Money Morning