For a nascent industry, ‘Buy now, pay later’ (BNPL) sure has a turbulent history.

From humble beginnings as a fledgling sector catering largely to local fashion retailers, BNPL quickly grew into big business.

Almost in no time at all, one of the industry’s leaders — Afterpay — got acquired in the biggest takeover deal in Australian history.

Everything seems to happen at warp speed with BNPL: both the ascent of BNPL as a payment method and the crash of BNPL stocks.

And while interest-free instalment payments are unlikely to go away, one question continues to plague the sector.

Can BNPL stocks ever become profitable? Is a standalone BNPL model sustainable?

High growth and high losses

In their heyday, BNPL stocks excited investors with their continued strong top-line growth.

And the growth has been impressive.

Consider Afterpay’s 2016 prospectus. In it, the BNPL firm reported H1 FY16 underlying merchant sales (the total volume of transactions processed) of $6.5 million.

In FY17, that figure jumped to $561 million.

By FY21, underlying merchant sales were $21.1 billion.

So between FY17 and FY21, Afterpay’s total transaction volume increased by more than 4,000%.

No wonder the market decided to pay up for that growth.

But that growth came at a cost.

In FY17, Afterpay reported a net loss of $9.6 million on operating cash outflows of $78.8 million.

By FY21, APT’s net loss was $160 million on operating cash outflows of $571 million.

It’s been a similar story for Afterpay’s nearest rivals like Zip, Sezzle, and Klarna.

BNPL stocks target profitability

Despite the growing losses, BNPL stocks believe they can be profitable long term.

Here’s what Afterpay said in its FY21 report:

‘The Company believes there is significant scope to increase revenue and profitability from its business strategy. The Company’s focus is to deliver long-term returns, strong revenue growth and profitability to shareholders by increasing the number of underlying Afterpay sales and Afterpay merchant fees.’

Yet Afterpay didn’t say that in FY21…it said that in its FY17 report.

ZIP was equally upbeat about profitability in its FY17 report, writing:

‘We face FY18 as a strong, rapidly growing, agile company firmly focussed on the profitable expansion of our Australian business through delivery of our omni-channel credit, payments and PFM strategies.’

But since FY17, profitability has been further away, not closer.

BNPL and bad debts

While BNPL stocks talk about their economies of scale and high asset turnover, their margins remain very thin.

For instance, in FY21, Afterpay’s net margin was just above 2%.

Yet with margins already thin, BNPL firms also have to contend with high bad debts and transaction losses.

If we take Afterpay as an example again…

In FY21, Afterpay reported $195 million of receivables impairment expenses on income of $822 million.

Bad debts continue to be a problem.

Just this week, Businessweek ran a cover story on the sector, heavily focusing on BNPL’s problem with bad debt:

‘A recent study by economist Amy Crews Cutts showed 17% of BNPL borrowers used the service after maxing out their credit card, and almost half made purchases they acknowledged they couldn’t otherwise afford. In a survey of more than 1,000 users, one-third told Credit Karma they’d fallen behind on payments.’

And with growing competition set to shrink merchant fees, BNPL margins can fall further.

Afterpay is well aware of this, writing in its 2016 prospectus (emphasis added):

‘Afterpay’s profitability depends on its ability to put in place and optimise its systems and processes to make accurate real time fraud and repayment capability assessments in connection with the end-customer approval process.

‘Afterpay already has exposure to end-customer bad debts as of the normal operation of its business. However, excessive exposure to bad debts through customers failing to meet their repayments to Afterpay will materially and adversely impact Afterpay’s profitability.’

Capital recycling: how BNPL stocks make money

So how can BNPL stocks ever become profitable?

The key lies in what’s called capital recycling — or how quickly BNPL stocks can turn over their receivables.

As chartered accountant Jason Andrew explained in SmartCompany:

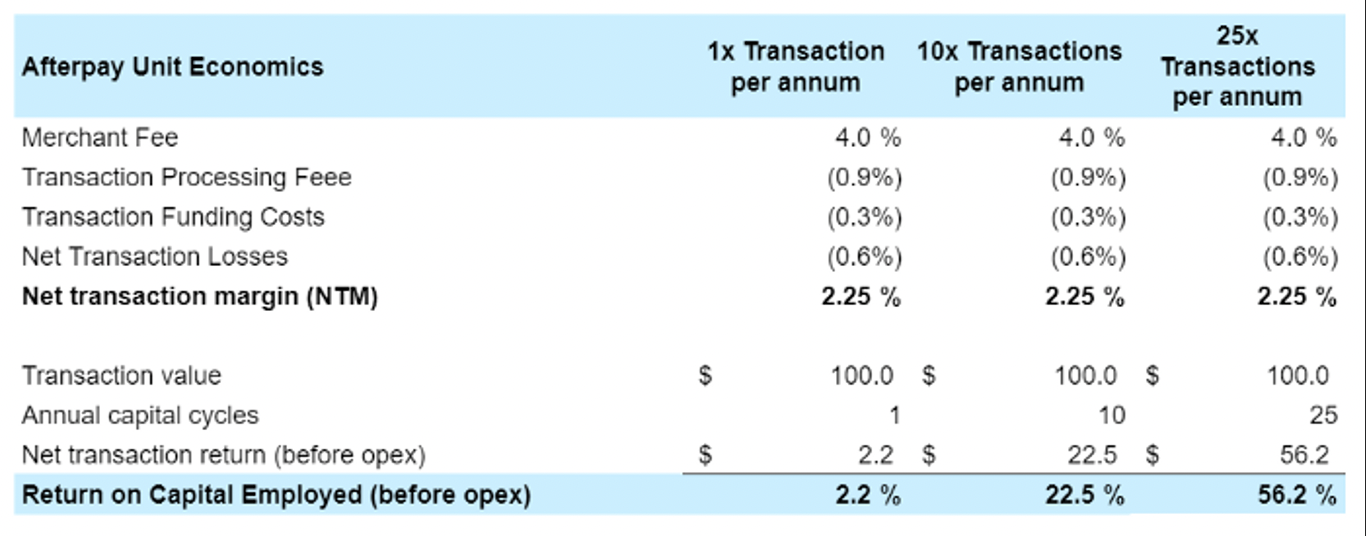

‘To put this in practical terms, let’s assume that a consumer spends on average $100 per transaction via Afterpay.

‘If this consumer only uses Afterpay once per year, Afterpay makes $2.25 per year of transaction margin and a 2.25% Return on Capital (ROC) before operating expenses.

‘But if the consumer uses it 10 times per year, Afterpay makes $22.50 per year. The initial $100 of capital that Afterpay borrowed is redeployed every time a new transaction is made. The return on capital is now 22.50% because the same $100 is now generating $22.50 of annual net transaction dollars.

‘In its FY20 report, Afterpay reported that its longest cohort of users are transacting up to 25x per annum — which implies that Afterpay could be generating a whopping 56% of ROC per annum on its oldest users.’

|

|

|

Source: Jason Andrew |

That’s backed up by research from McKinsey. In a June 2021 report, McKinsey found:

‘Given the shorter duration of financing in this model, receivables turn over about eight to ten times a year, resulting in return on assets (ROA) between 30 and 35 percent.’

Clearly, however, the high ROA is still not enough for most of the BNPL stocks, whose losses continue to mount.

So what’s the necessary ROA for the BNPL industry?

BNPL’s critical mass

BNPL stocks like Afterpay and Zip often talk about the network effects and economies of scale that should supposedly eventuate from rising customer numbers and transaction volumes.

Reach a certain number of customers and hit a certain transaction volume level, the theory goes, and profits should take care of themselves.

But what is BNPL’s critical mass?

At what level of transaction sales volume does a BNPL business become profitable?

In its prospectus, Afterpay hitched its profitability exclusively to growth in its merchant sales (emphasis added):

‘Afterpay is currently in the early stages of establishing its presence in the Australian market, and its ability to profitably scale its business is heavily reliant on increases in transaction volumes and in its end customer and retail merchant client base to increase revenues and profits. Failure to expand in this way may adversely impact Afterpay’s ability to improve its future profitability.’

But if Afterpay is possibly generating more than 50% of ROC per annum on its most active users but still operating at a (growing) loss, what does it say about the sustainability of the BNPL business model?

Humm — the once-profitable BNPL company

Some readers may point to Humm as an example of how to run a profitable BNPL company.

Yet Humm — which once dubbed itself as the only profitable BNPL company in Australia — has seen its BNPL segment struggle in recent years.

So much so that Humm’s management decided to sell (unsuccessfully) the segment to Latitude Financial.

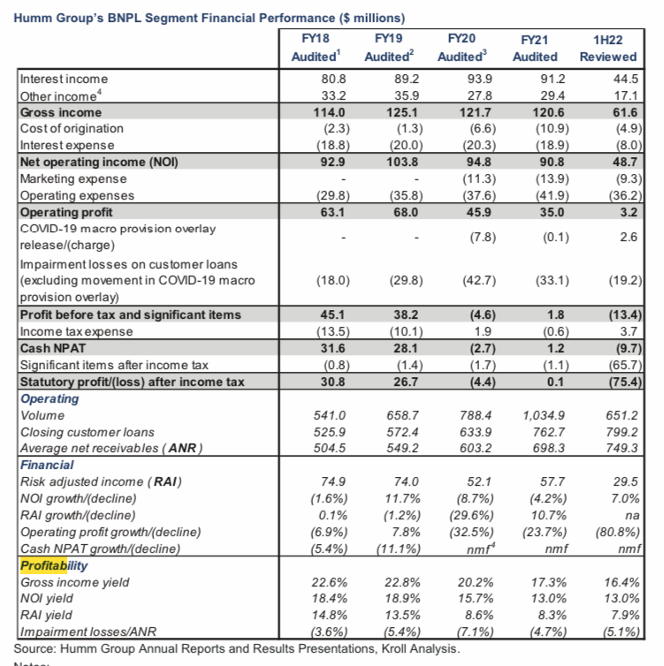

As an independent report on Humm’s BNPL segment found:

‘Cash NPAT fell from $31.6 million to $1.2 million between FY18 and FY21 due to the decline in operating profit over the period and the impact of investment in new products and offshore markets. Cash NPAT reached a loss of $9.7 million in 1H22 because impairment losses on customer loans exceeded operating profit during the period.’

|

|

|

Source: Humm |

Despite starting strong, Humm’s once-profitable BNPL segment was trending in the wrong direction.

So is the BNPL business model sustainable?

Time will tell, but the recent emphasis on cost-cutting and capital management by the sector suggests it is keenly aware it’s now or never.

Regards,

Kiryll Prakapenka,

For Money Morning