Explosives, chemicals, and fertiliser manufacturer Incitec Pivot [ASX:IPL] released an Investor Day Presentation and a run-down on FY22 results.

Incitec said FY22 earnings were ‘benefitting from the favourable commodity cycle, but somewhat impacted by certain other events’.

Over the past 12 months, IPL shares are up 40%.

Source: www.tradingview.com

Incitec’s investor day

On Tuesday, Incitec released its investor day presentation.

Included in the presentation was its FY22 business performance update.

For its Dyno Nobel segment, Incitec reported above market growth in quarry, construction, and coal during FY22.

The same couldn’t be said for IPL’s metals production, hindered by an outage at one of the company’s customer plants.

Since its restart, the WALA segment has been working above nameplate, with insurance proceeds expected sometime this month.

Dyno capital remains on plan, although IPL’s explosives segment has run into supply chain disturbances, and inflation has put notable pressure on operations, recovery, and pricing.

Due to equipment-sourcing difficulties, the company expects the Cheyenne project’s turnaround to be delayed into 2023.

For Incitec’s DNAP segment, the company reported negative impacts caused by bad weather conditions and further supply chain issues. Having said that, working capital is tracking ‘slightly above plan’.

As for Incitec’s fertilising business, the company declared farming conditions were favourable, and working capital remains on target.

The company completed its Phosphate Hill turnaround, bringing the plant to nameplate standard, and is now estimating around 750 kt in annual production volume for FY22.

There was a gas supply disturbance at Phosphate Hill, which inflated gas costs by around AU$45million. However, the company expects services to be restored by February 2023, and measures have been taken in the interim.

Fertilising demand has been lower than usual, so distribution has dwindled. Incitec believes this is yet another example of inflationary pressure pushing up prices, and supply issues playing a part. EBIT is now forecast between the range of AU$40–45 million for FY22.

Gibson Island will be discontinuing manufacturing at the end of the year, and general closing costs remain in line with previous estimates:

Source: IPL

Outlook for IPL

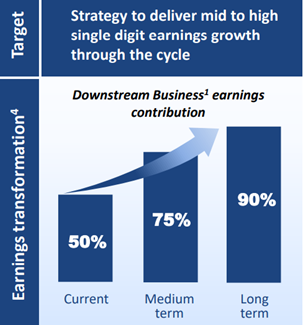

Incitec intends to find ways to accelerate its earnings (targeting mid-to-high single-digit underlying earnings growth), achieve capital returns and hit sustainability targets for FY23.

Further to these goals, IPL said it would look for investment opportunities through prioritised outlets and focus on decarbonised ammonia upstream to hit ‘net-zero’ targets.

Incitec said it was encouraged by nitrogen and phosphate market movements and claims resilience in the nitrogen market, with 66% nitrogen being internally sourced. IPL also says that its earnings trajectory has proven ‘less exposed to commodity cycles’:

Source: IPL

IPL also feels boosted by ‘improved earnings and predictability driving results through the cycle’, with projects aligned to hit new targets in 2023.

Incitec appears particularly excited about where its Dyno segment is headed in the next financial year, a ‘strong balance sheet’ expected to drive investments planned in North and South America, Asia, Europe, Africa, and Australia:

Building wealth in a bear market

Incitec has been affected by inflation, just like many other businesses.

So, is it even possible to build wealth or even plan for retirement in these times?

If you’ve been unsure about what strategies could possibly work right now, you might like to check out our free event, ‘The 30% Next Egg’ this Thursday night.

Our esteemed trading guru Murray Dawes will share his simple strategies for conservative investors who hope to boost their nest egg savings.

To book your spot at the free event, click here.

Regards,

Kiryll Prakapenka,

For Money Morning